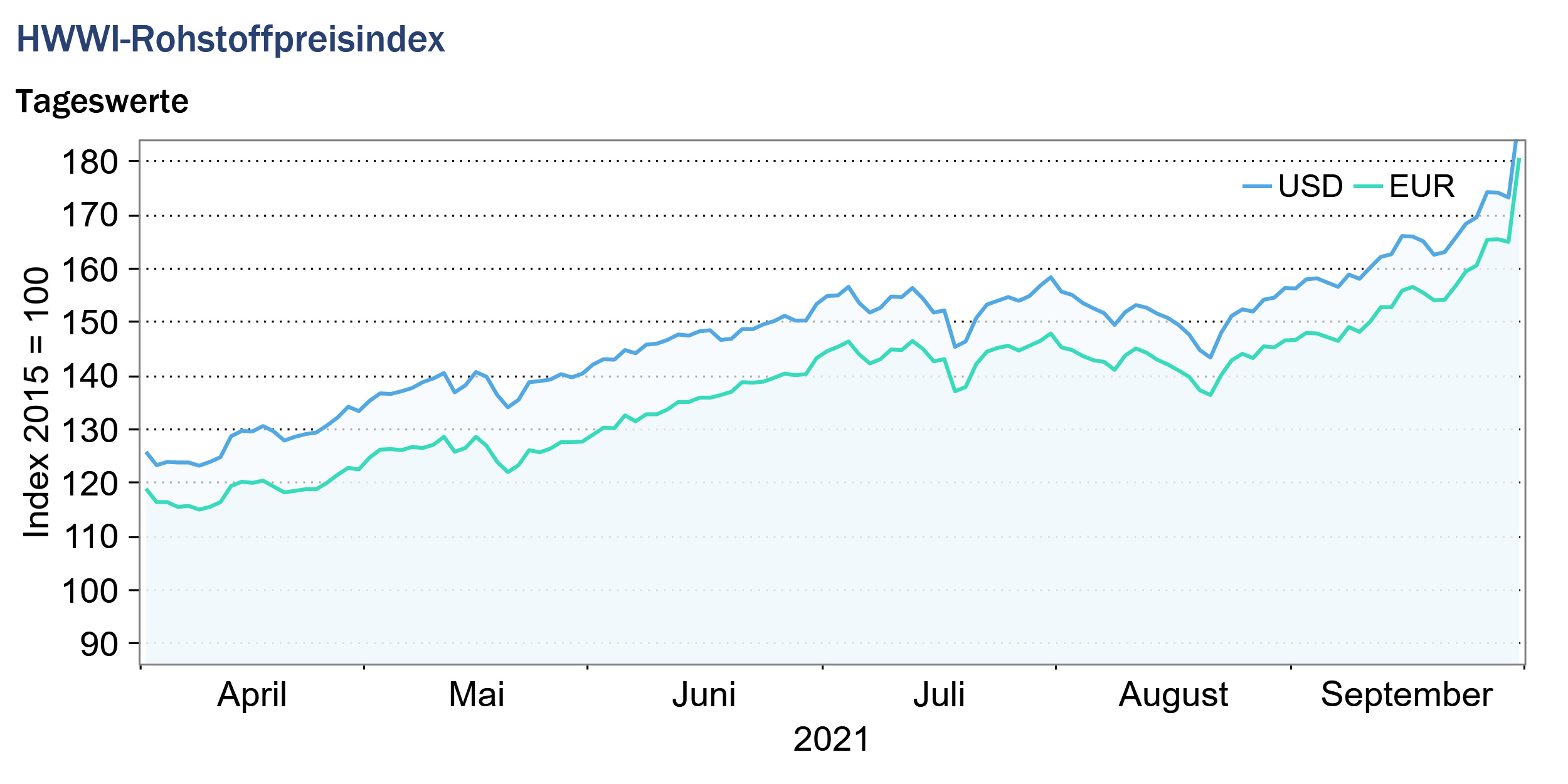

Strong rise in energy commodity prices

- HWWI overall index rose 8.8% (U.S. dollar basis)

- Crude oil prices rose 5.3%

- Natural gas prices increased by 31.1%

(Hamburg, October 12, 2021) The HWWI commodity price index increased by an average of 8.8% in September compared to the previous month and was 91.5% higher than the corresponding figure for the previous year. The increase in the HWWI Commodity Price Index was due to strong price increases in energy commodity markets. In addition to coal and natural gas prices, crude oil prices also rose sharply in September. The background to the price increases is that increased demand for energy raw materials in the wake of the global economic recovery is currently being offset by a shortage of supply. The strongest price increases were recorded on the markets for European natural gas, reflecting the empty natural gas storage facilities in Europe. In contrast, prices for industrial commodities and food and beverages fell on average in September.

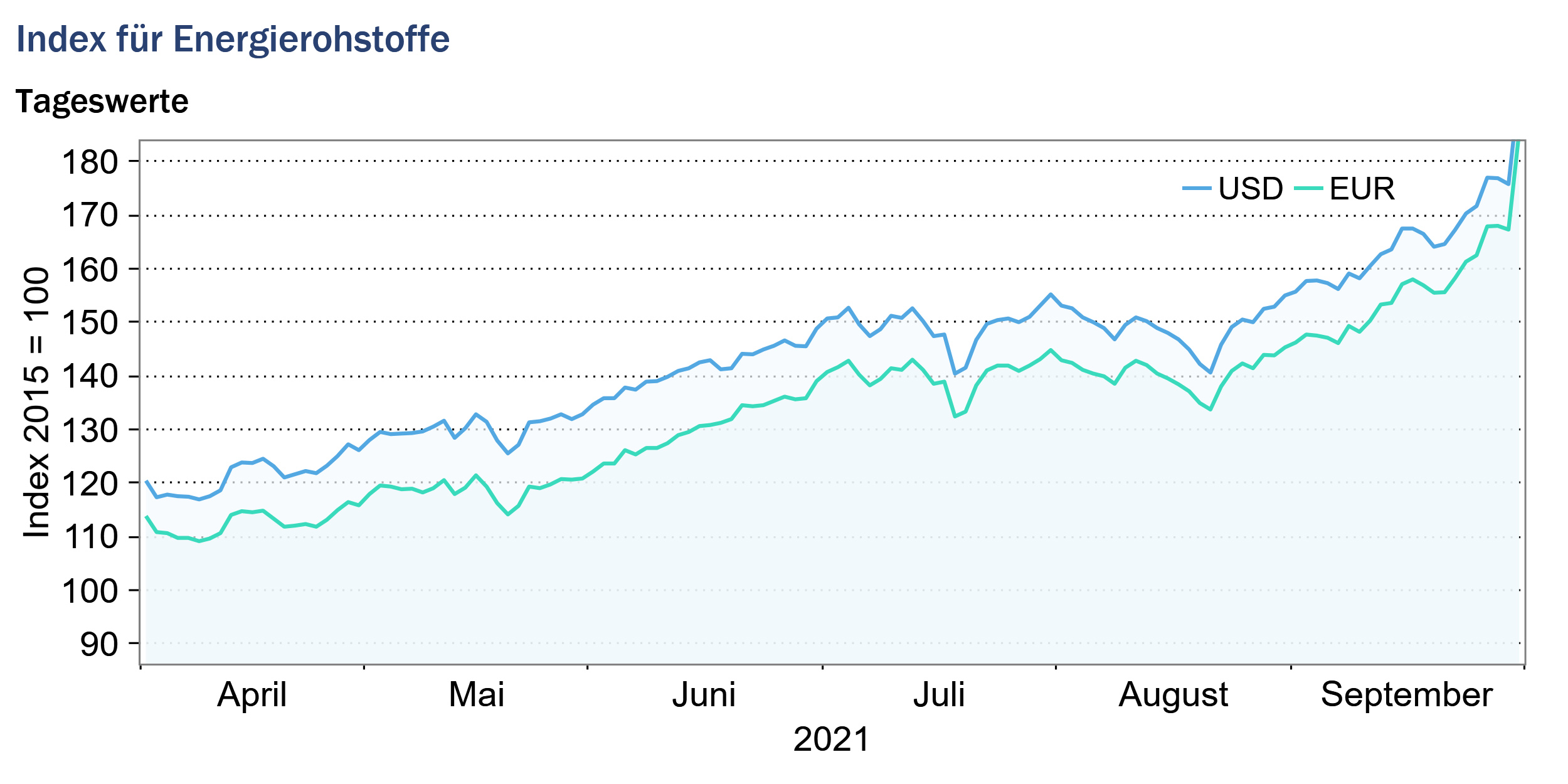

Index for energy commodities: +11.3% (euro basis: +11.4%)

In the crude oil markets, a clear upward trend in oil prices was observed in September. At the end of the month, prices for European reference Brent crude approached the $80 per barrel mark, which had not been exceeded since 2018. U.S. benchmark WTI ended the month at $75 per barrel. Compared to September 2020, crude oil prices increased by more than 77% on average. The price increases were due to increased demand for crude oil because of the global recovery following the Corona recession, combined with tight supply. Despite the sharp rise in prices, OPEC+ announced that it would stick to its production policy and not expand supply further than planned. OPEC+, which is currently benefiting from high crude oil prices, justified its action by citing uncertainty about a fourth Corona wave, which could again depress demand for crude oil.

Coal and natural gas prices also continued their strong upward trend in September. The increased prices for coal and natural gas are due to a sequence of events that increased demand, as well as tightened supply. A key price driver is increased demand for electricity from China, triggered by the economic recovery from the Corona pandemic and a hot spell that caused a sharp increase in demand for electricity for air conditioning. A decline in the supply of hydroelectricity due to a drought in China further increased Chinese demand for energy commodities such as coal and natural gas, which was reflected in increased import demand. Other economies also saw an increase in demand for coal and natural gas because of the recovery of the global economy, which drove up prices.

Prices for European natural gas reached historic highs in September and were more than four times higher than in September a year earlier. Natural gas storage facilities in Europe were already heavily depleted because of the long, cold winter of 20/21 and could not be fully replenished due to increased demand. In addition, the supply of natural gas in Europe has decreased. In particular, the Netherlands, a major producer of natural gas in the European Union, had to severely curtail natural gas supplies due to earthquake risks.

Overall, the energy commodities sub-index rose 11.3% (euro basis: 11.4%) to 166.0 points (euro basis: 156.5 points).

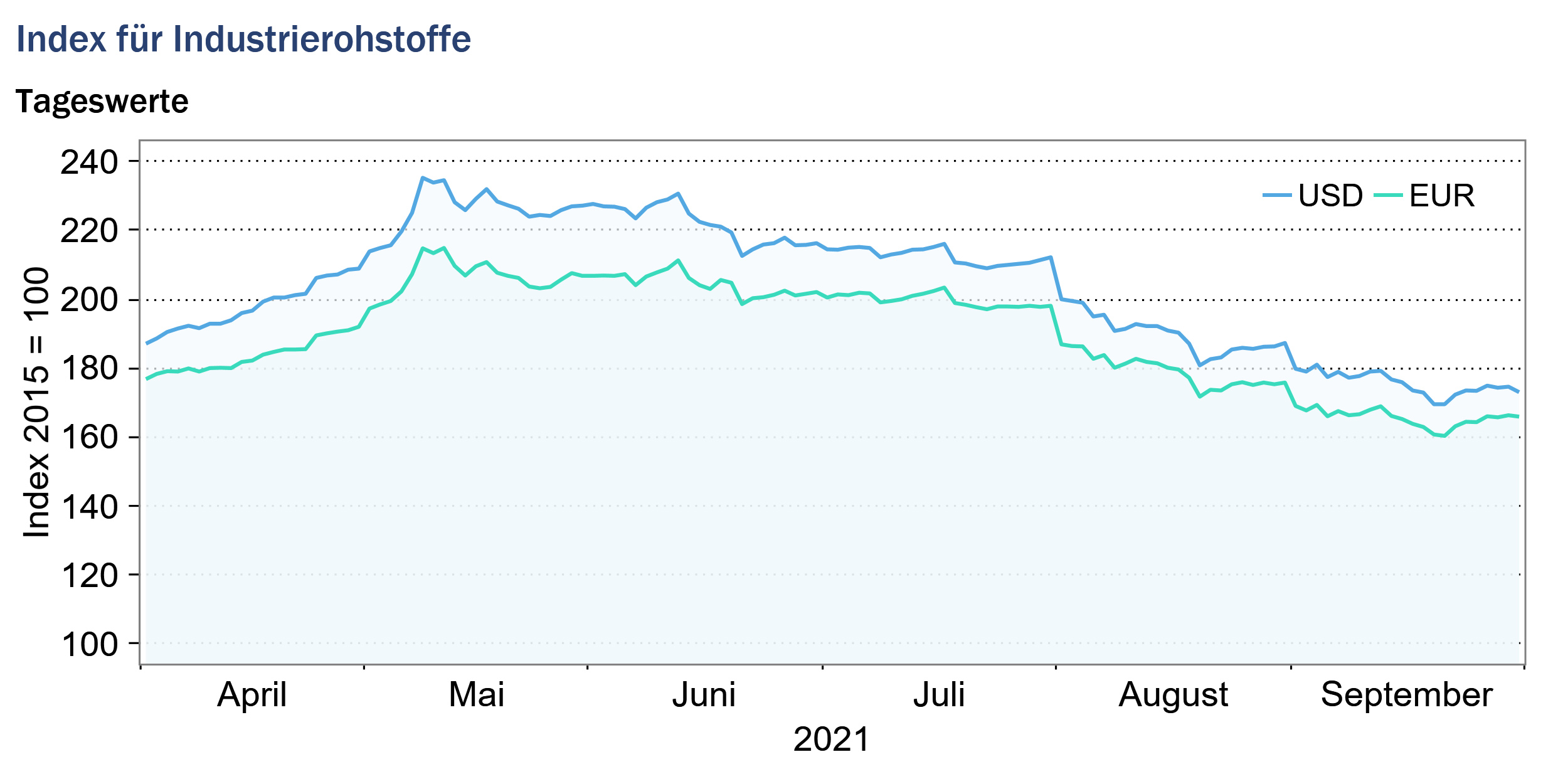

Index for industrial raw materials: -7.6% (euro basis: -7.6%)

The industrial commodities sub-index, which is divided into the agricultural commodities index, the nonferrous metals index, and the iron ore and steel scrap index, fell 7.6% in September from the previous month.

The iron ore and steel scrap sub-index continued its downward trend in September, falling another 21.6% from the previous month. China, the world’s biggest iron ore consumer, curtailed its iron ore imports as Chinese steel production was sharply reduced due to climate protection measures. In addition, the imminent collapse of the major Chinese real estate company Evergrande created uncertainty about the future of the Chinese construction sector and thus about the future development of steel consumption.

Aluminum prices continued to rise in September. Aluminum supply continues to suffer from power shortages in China, which ensured that energy-intensive aluminum production was reduced. China’s goal of cutting emissions also implies that production will not be expanded further for the time being. Aluminum prices rose 8.6% in September from the previous month and were almost 63% higher than the corresponding year-earlier levels.

Lead prices, on the other hand, fell in September from the previous month after rising in August due to supply chain disruptions. While inventories were historically low last month on the London Metal Exchange (LME), the Chinese exchange, the Shanghai Futures Exchange (SHFE), recorded high stocks of lead. Panic buying occurred on the spot market, as evidenced by the high price differentials between contracts for immediate delivery and contracts for later delivery on the LME. Immediate delivery of the commodity was significantly more expensive than delivery later. In September, the situation eased and lead prices eased again.

Despite uncertainty about the future impact of the impending Evergrande bankruptcy on demand for industrial metals, prices for nickel, zinc and copper remained at a high level and recorded only moderate price fluctuations on average in September. Nickel and zinc prices recorded a slight increase in September, while copper prices fell slightly on average for the month.

Overall, the index for industrial raw materials fell by -7.6% (euro basis: -7.6%) to 175.6 points (euro basis: 165.6 points) on a monthly average.

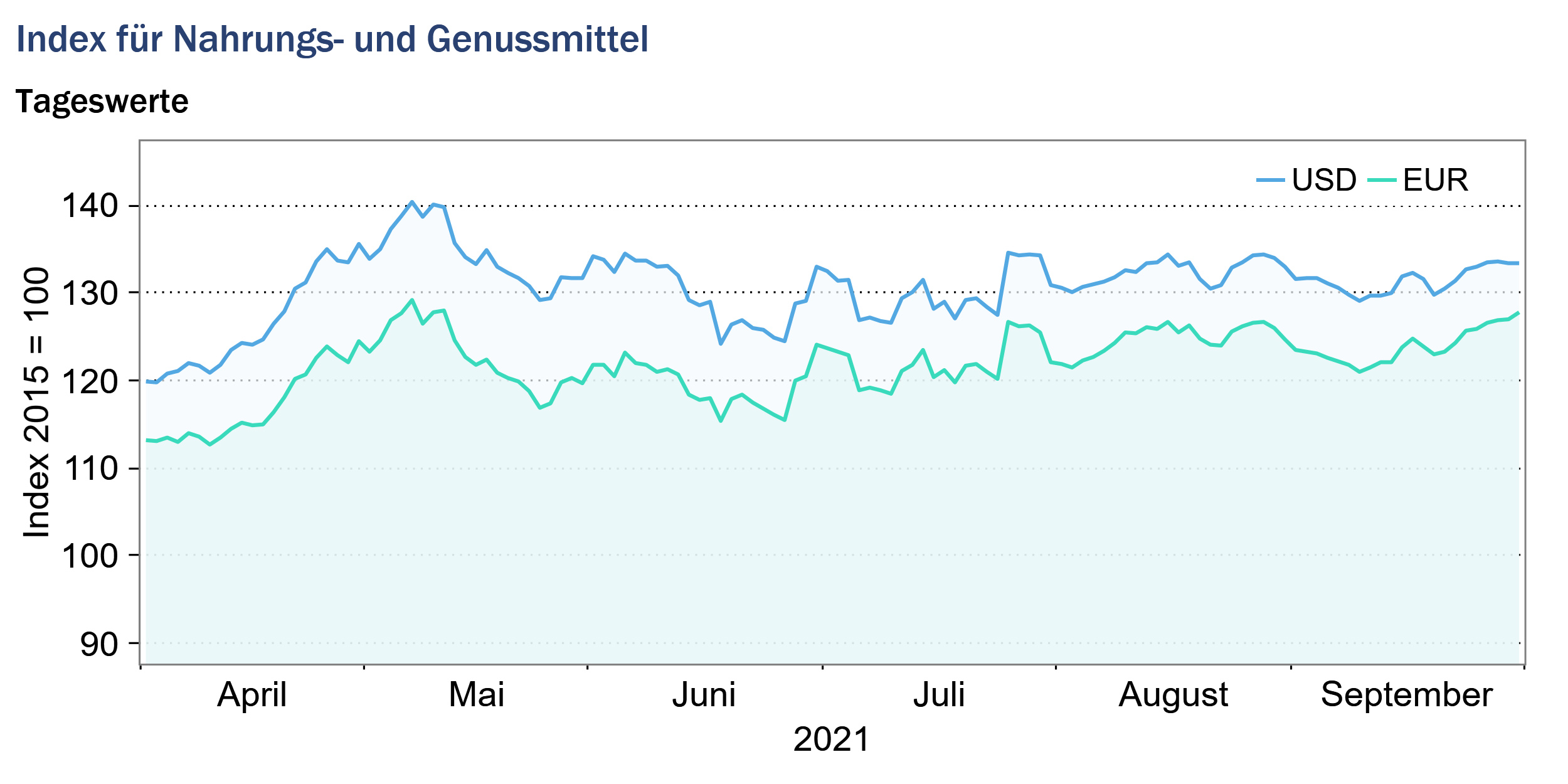

Food & Beverages Index: -0.7% (euro basis: -0.7%)

The index for food, beverages and tobacco fell by an average of 0.7% in September compared with the previous month and was 32.5% higher than the corresponding year-earlier figure. While prices for cereals and vegetable oils fell slightly, prices for luxury foods rose slightly in September.

Wheat and barley prices remained at a high level in September, but the strong price increase of the previous month did not continue. Barley, for example, recorded only a slight price increase, and wheat prices fell slightly on average for the month compared with the previous month.

Corn and rice prices fell on average in September from the previous month. Upward pressure on corn markets, triggered by port disruptions following hurricanes in the U.S., was offset by improved global crop prospects. Palm oil prices, on the other hand, rose for the third consecutive month, reaching a ten-year high. Palm oil prices continue to be supported by robust global import demand. In addition, supply of palm oil from Malaysia remains tight as production in Malaysia continues to suffer from a labor shortage due to the Corona pandemic.

Prices for luxury food products, particularly coffee and cocoa, continued to rise in September compared with the previous month. For example, coffee prices averaged almost 50% higher for the month than in September 2020. The price increase was due to poor crop forecasts from Brazil. The Brazilian coffee crop was significantly impacted by a severe drought early in the season and later by intense frosts. Cocoa prices reacted to heavy rains in Côte d’Ivoire, which triggered an outbreak of a fungal disease harmful to cocoa plants in some growing regions.

Overall, the food and beverages index fell 0.7% on average for the month (euro basis: -0.7%) to trade at 131.5 points (euro basis: 123.9 points).

Source: www.hwwi.org