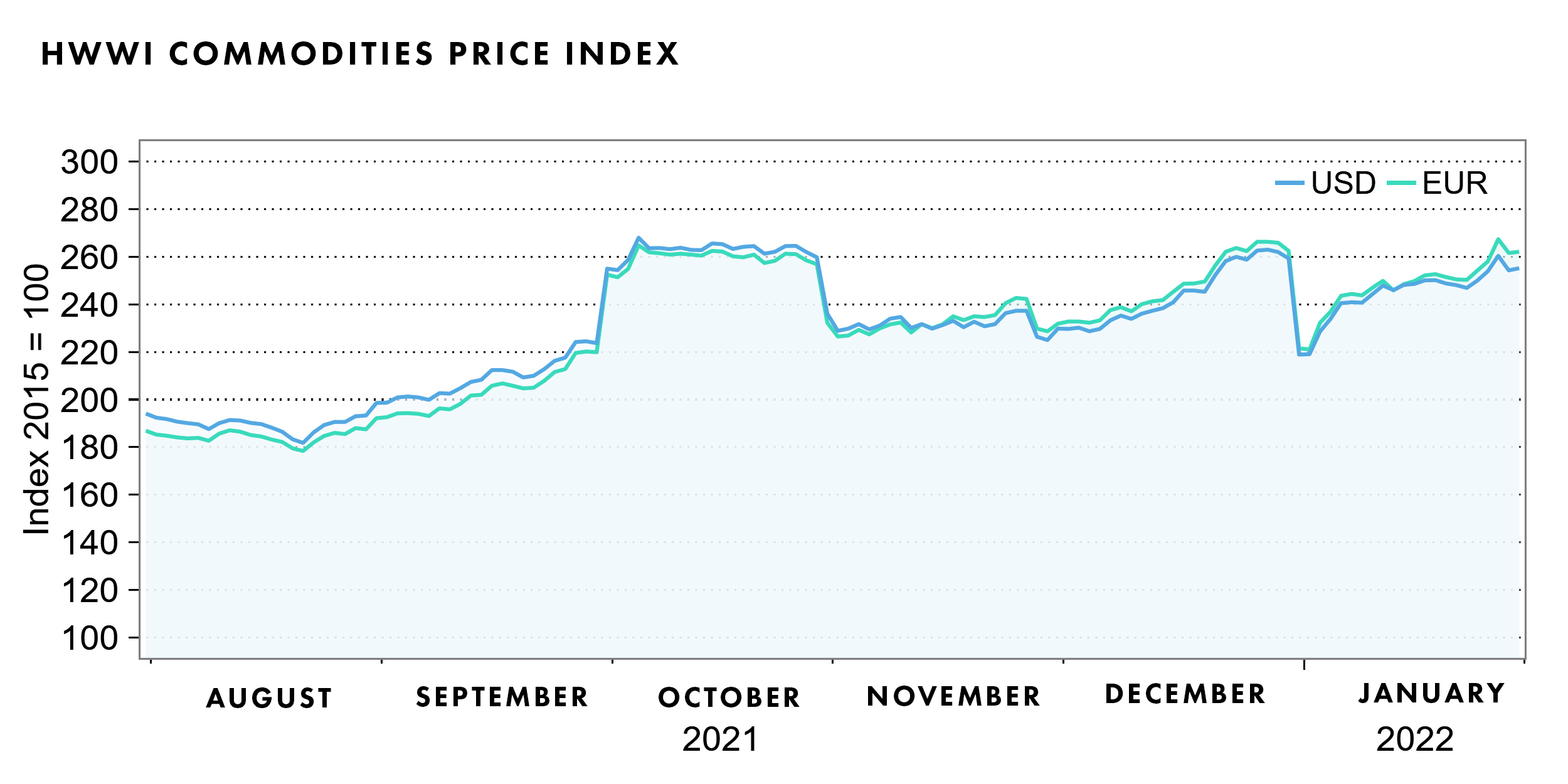

HWWI commodity price index records slight increase in January

- HWWI overall index increased by 0.7 % (US dollar basis)

- Crude oil prices increased by 14.4

- Natural gas prices fell by 17.7

(Hamburg, February 10, 2022) The HWWI commodity price index rose only slightly by 0.7% on average in January compared with the previous month. Compared with the previous month, the index for energy commodities recorded a slight decline of 0.3% on average in January, due to price losses on the markets for European natural gas. By contrast, prices for coal and crude oil rose sharply in January compared with the previous month. The markets for industrial raw materials also saw price increases in January. Prices for both industrial metals and agricultural industrial raw materials, such as wood, continued their upward trend. Prices for food and beverages also increased in January compared with the previous month, with prices for oilseeds and oils in particular rising sharply.

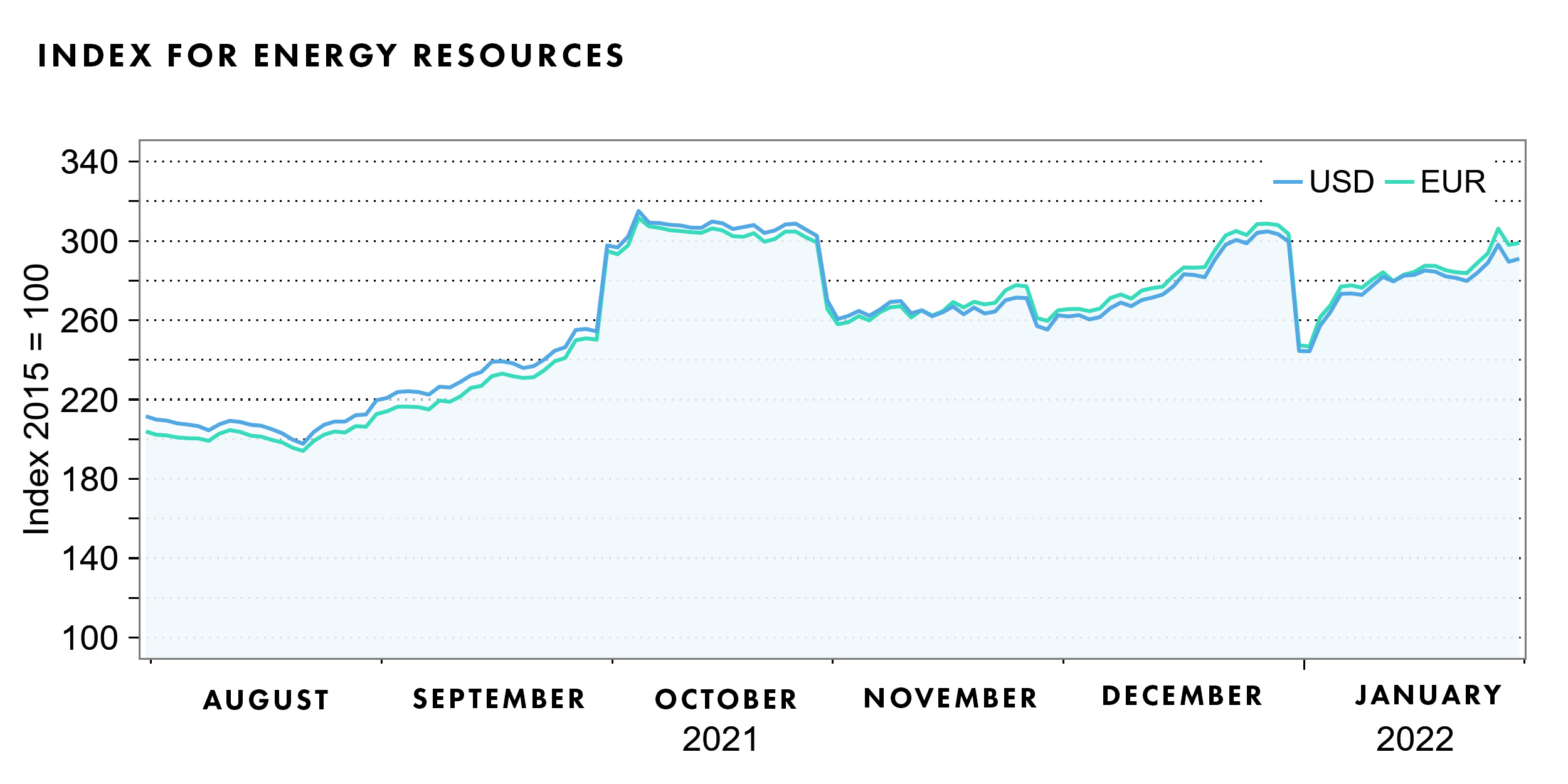

Energy commodities index: -0.3% (euro basis: -0.5%)

Crude oil prices again rose significantly in January despite the Omikron virus variant spreading further. Thus, the prices of the European Brent crude oil grade ended the month at highs of 91 U.S. dollars per barrel and the prices of the U.S. WTI crude oil grade at 89 U.S. dollars per barrel. Crude oil prices of both grades thus reached highs last seen in 2014. The rise in crude oil prices is attributable to concerns about a supply shortage. On the one hand, a cold snap in Texas is raising concerns about shale oil production outages. On the other hand, political tensions between Russia and Ukraine are affecting the crude oil market. Russia is a major crude oil producer and an escalation of the conflict could affect crude oil supplies from Russia. Despite the rapid spread of the omicron variant, demand for crude oil remained stable.

Coal prices also continued their upward trend in January. While South African coal prices increased by 21% from the previous month, Australian coal prices rose by as much as 27%. A temporary export ban by Indonesia, a major coal supplier, tightened supply on the world markets in January and drove up coal prices.

The picture on the natural gas markets at the beginning of the year was somewhat different from previous months. Compared with December, prices for American natural gas rose by 10%, while prices for European natural gas fell by 22%. Due to tight European gas supplies and the current tensions between Russia and Ukraine, European LNG imports from the USA increased significantly in January. As a result, prices for American natural gas rose, while prices for European natural gas fell. The relatively mild weather also eased the situation on the European natural gas market. In January, European natural gas prices were lower than in December but still at a very high level. As before, the European natural gas market remains tense due to geopolitical tensions between Russia and Ukraine.

Overall, the energy commodities sub-index fell by 0.3% (euro basis: -0.5%) to 278.8 points (euro basis: 282.5 points).

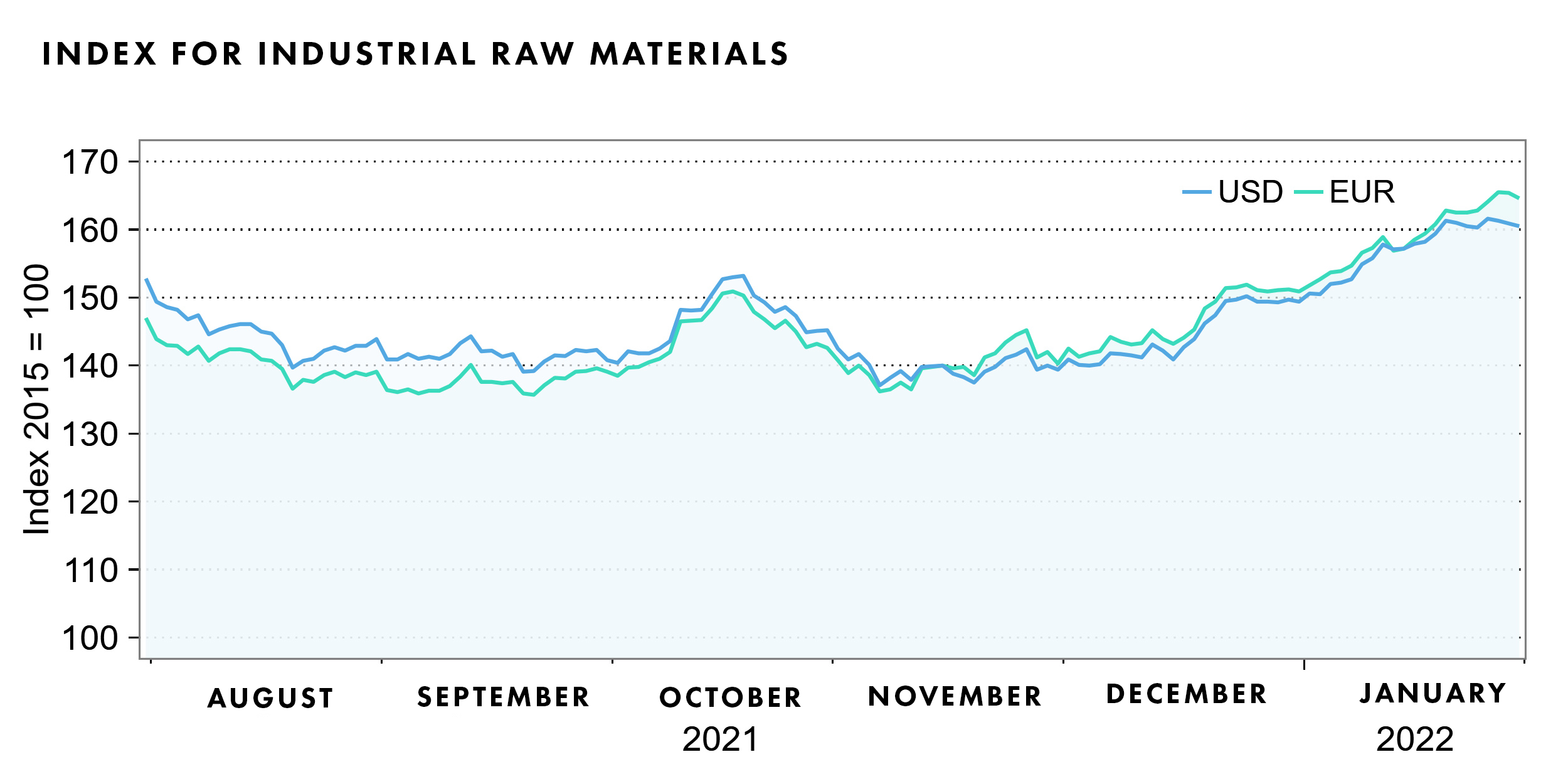

Index for industrial raw materials: +8.6% (euro basis: +8.6%)

The industrial raw materials subindex, which is broken down into the index for agricultural raw materials, the index for nonferrous metals and the index for iron ore and steel scrap, rose by 8.6% in January compared with the previous month. All three sub-indices recorded increases on average for the month.

After falling significantly in previous months, iron ore prices increased by 17% in January from the previous month, but on average remained well below the level of the corresponding month a year earlier. The higher price reflected an increase in demand coupled with a shortage of supply. Demand for iron ore was fueled by the Chinese steel industry. Chinese steel production has been repeatedly curtailed in recent months to reduce the country’s CO2 emissions. Especially before the Olympic Games, the Chinese government wanted to reduce pollution. Steel production is expected to increase again after the Olympics. In contrast, the supply of iron ore has been strained by the spread of the Omikron virus variant in Australia. Australia is one of the world’s largest iron ore producers, and further spread of the Omikron virus could lead to significant production disruptions.

Prices for non-ferrous metals also recorded increases in January. Aluminum and nickel prices rose particularly sharply in January; both prices increased by over 10% from the previous month. Lockdown measures to combat the current spread of the Omikron virus in China are currently affecting the supply of aluminum. Threats of sanctions against Russia, another major aluminum producer, are also increasing concerns about a supply shortage. Nickel prices were also at levels not seen in 10 years and are being driven in part by increased demand for electromobility.

Prices for lumber also continued to rise strongly in January, increasing by a further 36% from the previous month. On the one hand, demand for lumber increased as construction activity is running at full speed, particularly in the USA. On the other hand, supply was restricted by disruptions in the supply chain due to extreme weather conditions, but also by labor shortages as a result of the Omikron virus.

Overall, the index for industrial raw materials rose by +8.6% (euro basis: +8.6%) to 157.3 points (euro basis: 159.2 points) on a monthly average.

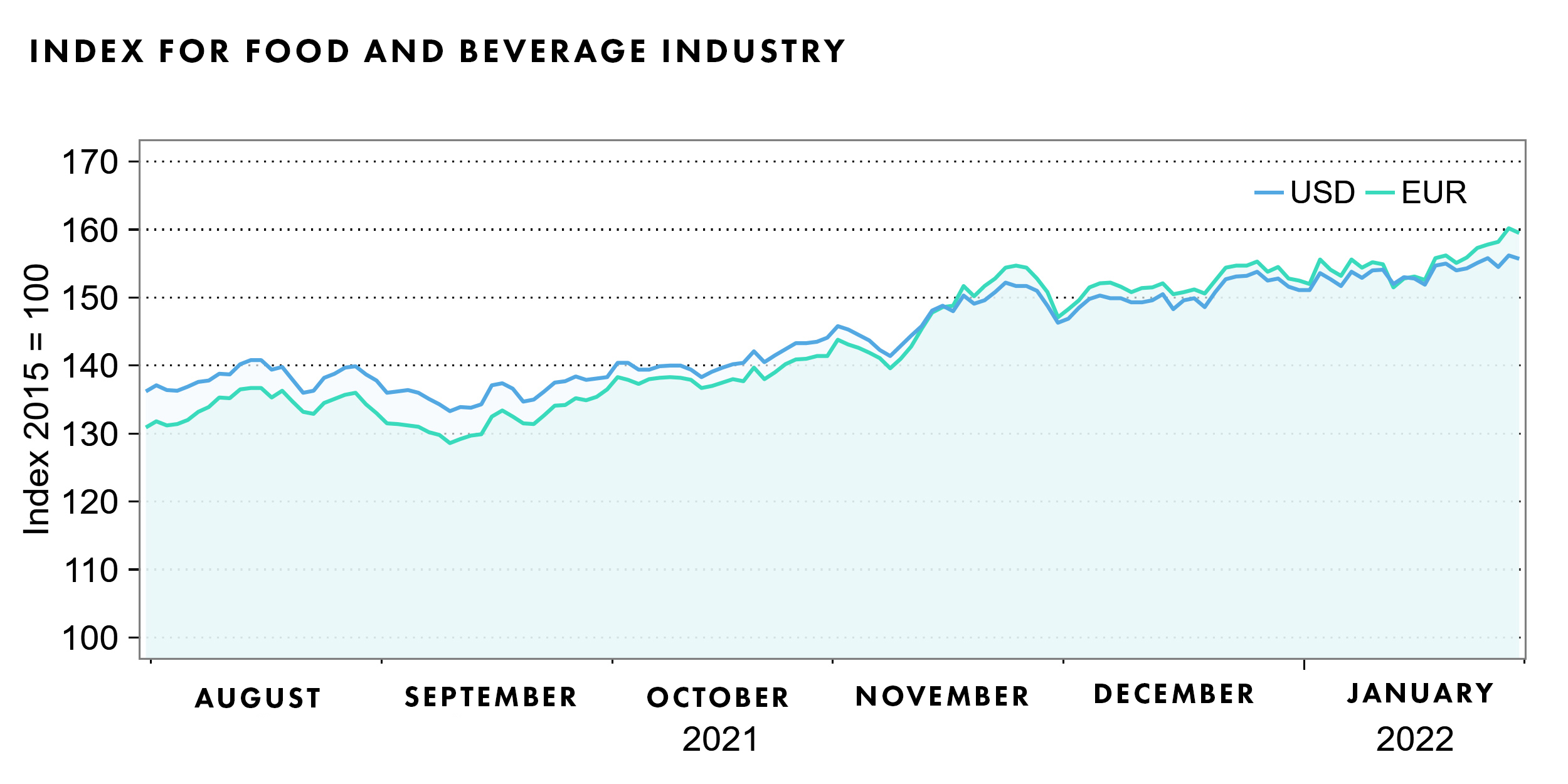

Index for food, beverages and tobacco: +2.1% (euro basis: +2.1%)

The index for food, beverages and tobacco rose by an average of 2.1% in January compared with the previous month and was thus 20.4% higher than the corresponding year-earlier figure. All three sub-indices, the index for cereals, the index for luxury foods and the index for oils and oilseeds, rose in January compared with the previous month.

In the cereals markets, rice prices in particular rose in January, while wheat prices fell. Higher rice prices reflected transportation bottlenecks in India, the world’s largest rice exporter.

The index for oils and oilseeds rose 6.5% in January from the previous month. Soybean prices continued to rise sharply in January as forecasts for the Brazilian soybean crop were revised downward due to poor weather conditions. Tight supply combined with increased demand drove prices for vegetable oils, namely soybean, palm, coconut and sunflower oil, higher in January. Supply continued to be weighed down by a combination of supply chain disruptions, labor shortages and extreme weather conditions in growing regions.

Prices for luxury food products moved in opposite directions in January. While coffee and cocoa prices rose, sugar and tea prices fell from the previous month. World market prices for coffee rose only slightly on average in January, but remained at a high level last seen ten years ago. On a year-over-year basis alone, coffee prices in January 2022 averaged 76.51 percent higher than a year earlier. Coffee prices continued to reflect tight supplies, particularly from Brazil. The impact of extreme drought early in the season and subsequent frost on the Brazilian coffee crop resulted in high coffee prices. In addition, transport bottlenecks caused by the Corona pandemic tightened coffee supplies. As demand for coffee remained stable, the tightening of supply led to price increases.

Cocoa prices also continued to rise in January compared with the previous month, due to drought conditions in key growing areas of Côte d’Ivoire. The lack of rain affected the quality of cocoa beans and worsened harvest prospects. Sugar prices, on the other hand, continued to fall in January. The weather-related tightening of Brazilian sugar supplies was offset by sugar production from major sugar suppliers Thailand and India.

Overall, the index for food, beverages and tobacco rose by an average of 2.1% for the month (euro basis: +2.1%) and stood at 153.7 points (euro basis: 155.3 points).

Source: www.hwwi.org